Have you heard about the latest changes in payroll deductions under the Canada Pension Plan (CPP) for 2024? In September 2023, the Government of Canada announced its 2024 CPP and EI rates for employee and employer contributions. This is part of Canada’s larger CPP enhancement plan that began in 2019 to increase the max CPP contribution each year for the next seven years. That’s not all. Along with rising CPP rates, EI rates are also following an upward trend, with contributions seeing gradual increases each year.

What does this all mean for you as an employer, and how will this impact your business’s bottom line?

In this article, we’ll cover everything you need to know about CPP and EI rates in Canada, including CPP contribution rates, maximums, and exemptions in 2024. We’ll also go over how the government’s CPP enhancement plan will affect employer contributions in the coming years.

.webp)

What is the Canada Pension Plan (CPP)?

Let's start with the fundamentals. The Canada Pension Plan (CPP) is a compulsory, government-operated retirement pension scheme in Canada that offers essential financial assistance to retired, disabled, or deceased workers and their families. It is a monthly, taxable benefits plan that replaces part of a worker’s income when they retire and is financed through contributions from employers, employees, and self-employed individuals.

CPP benefits are overseen by Canada’s federal government and are accessible to all qualified Canadian residents. The following factors determine eligibility: age, employment history, and contributions made to the plan. Individuals who have contributed to the CPP for a minimum of one year are entitled to receive retirement benefits once they reach 65 years of age.

The amount of benefit a worker is entitled to receive is based on their average earnings and the duration of their contributions to the plan. In addition to retirement benefits, the CPP also extends survivor and disability benefits to eligible recipients.

Survivor benefits are allocated to the surviving spouse or common-law partner of a deceased contributor, while disability benefits are provided to contributors who are unable to work due to a severe, prolonged disability.

What is the Required Employer Contribution?

The Canadian government establishes minimum and maximum CPP contributions, as well as the rate of contribution. These figures vary year by year and dictate the contributions made by both the employee and the employer to the CPP. CPP max 2024 contributions were recently decided by the CRA – continue reading for more details on CPP and EI rates for 2024.

According to CPP regulations, both the employer and the employee must make contributions to the CPP when an employee is engaged in pensionable employment. It is the employer's responsibility to make CPP contributions for each individual they employ. This amount must be submitted to the Canada Revenue Agency (CRA) regularly. The employer and employee contributions to the CPP are equal. Meaning the employer and employee will both submit the same monetary amount at the required intervals.

How to Determine CPP Contributions

As an employer, it's your responsibility to subtract CPP contributions from your employee's pensionable earnings. CPP contributions are typically due on a monthly basis.

Employers are required to contribute an amount equivalent to the CPP deductions made from the employees' earnings and submit the total of both sums. This practice is maintained annually in accordance with the Canadian government's CPP enhancement plan.

The Government of Canada annually specifies the maximum pensionable earnings, the year's basic exemption amount, and the applicable rate for employers to use in computing the CPP contributions to be deducted from the employees' pay.

For instance, if we take the CPP contributions you as an employer are responsible for deducting from one month of an employee's salary ($240.40) and add your portion of CPP contributions ($240.40), the total sum is the total amount you'll remit for CPP contributions in that particular month ($480.80).

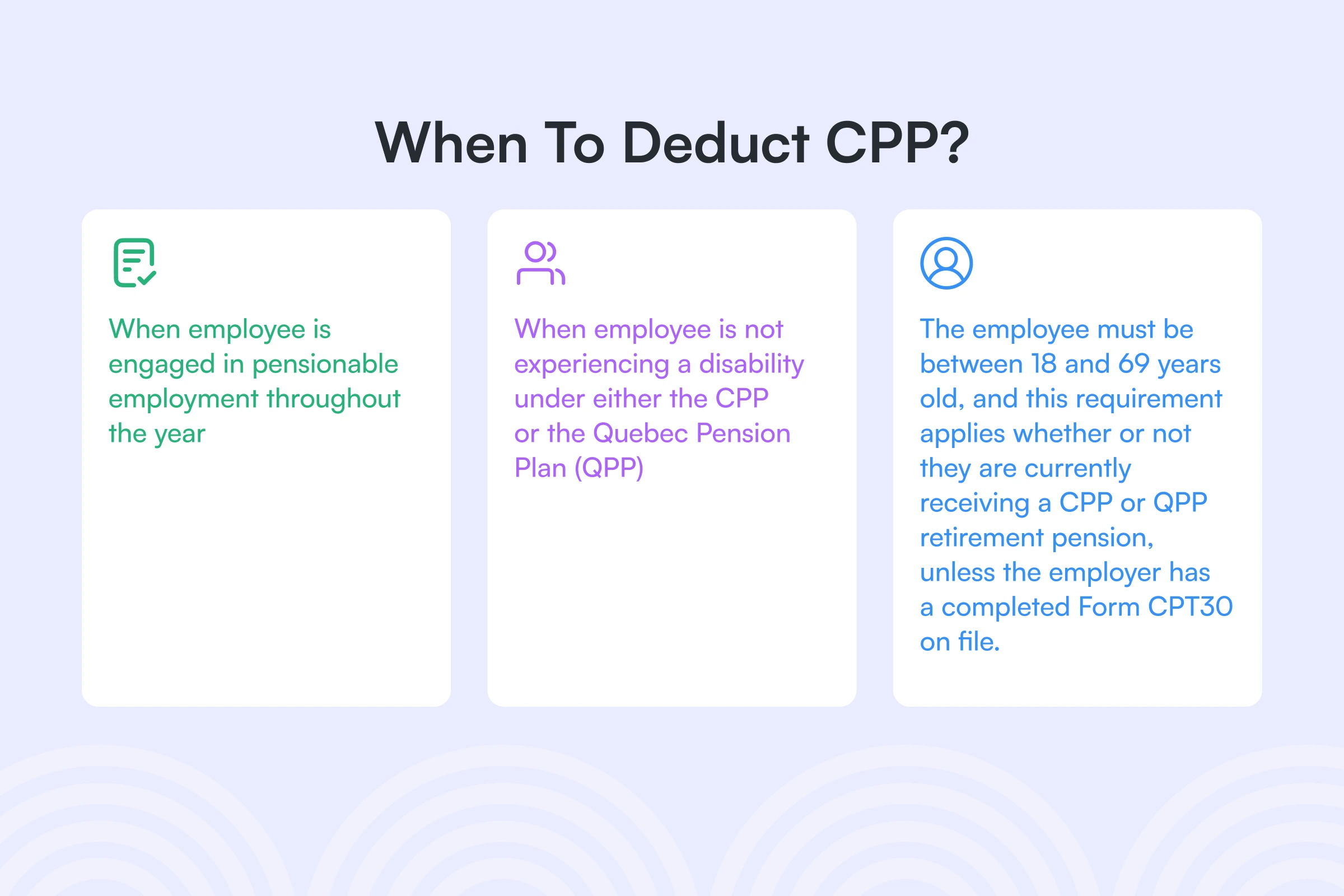

When to Deduct CPP

Employers are required to withhold CPP contributions from the employee's pensionable earnings if they meet the following conditions:

- The employee is engaged in pensionable employment throughout the year.

- The employee is not experiencing a disability under either the CPP or the Quebec Pension Plan (QPP).

- The employee's age falls within the range of 18 to 69 years, regardless of whether they are already receiving a CPP or QPP retirement pension (unless the employer receives a completed Form CPT30).

For businesses in Quebec, employers must deduct Quebec Pension Plan (QPP) contributions instead of CPP contributions. Maximum QPP contribution rates are typically higher than CPP contribution rates. For further details, refer to the Guide for Employers: Source Deductions and Contributions.

What are Pensionable Earnings?

Pensionable earnings is the remuneration an employee receives from a position or job that qualifies for pension benefits, with certain exceptions.

Typically, employers are required to deduct CPP contributions from:

- Salary, wages, or other forms of compensation

- Commissions

- Bonuses

- Most taxable benefits

- Honorariums

- Some tips and gratuities

When to Stop Deducting CPP Contributions

As an employer, you should stop deducting CPP contributions once your employee's annual employment income hits the maximum pensionable earnings or the maximum employee contribution for the year. The exact numbers for CPP max payment amounts, payroll deductions, and maximum contributions can be found on the Government of Canada’s website and is updated yearly.

The notion of the annual maximum pensionable earnings applies to each position held by an employee with different employers (each having a distinct business number). If an employee transitions from one employer to another within the same year, the new employer must deduct CPP contributions, regardless of whether contributions were made by the previous employer. This applies even if the employee has already reached their maximum contribution limit with their previous employer.

Regarding retirement, the standard retirement age in Canada as of 2023 is 65 years old. This means that many employees may choose to begin receiving government retirement benefits around this age. However, employees can start receiving pension-related benefits as early as 60 or as late as 70 years old. If you receive a completed Form CPT30 from an employee aged between 60 and 70, you should stop deducting CPP contributions for that employee.

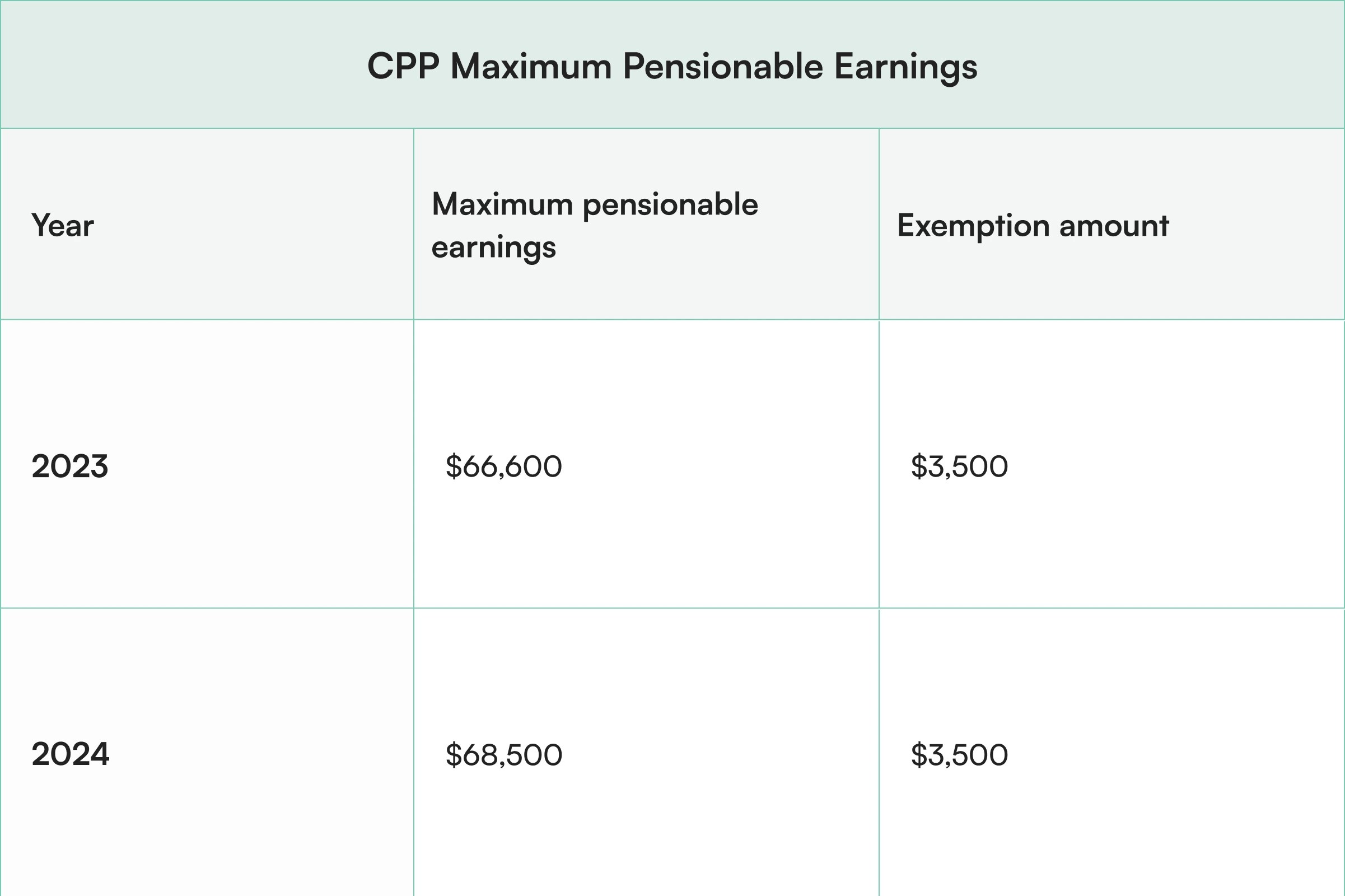

CPP Maximum Pensionable Earnings for 2024

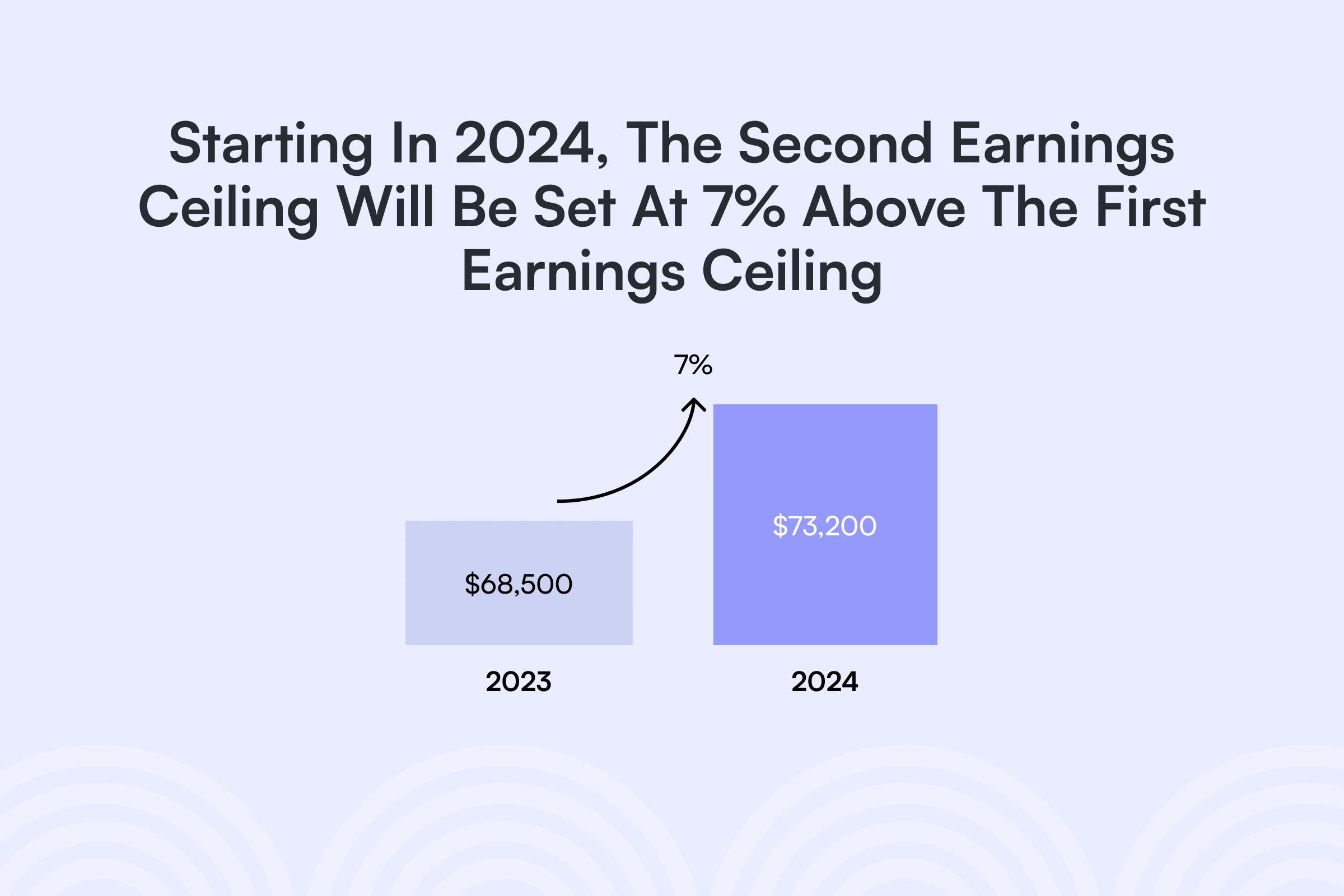

The maximum pensionable earnings, or first earnings ceiling (YMPE), in 2024 will be $68,500, up from $66,600 in 2023. The basic exemption amount for 2024 will remain at $3,500.

Starting in 2024, a higher second earnings ceiling (YAMPE) of $73,200 will be implemented as part of the CPP enhancement plan that will be used to determine a second additional CPP contribution (CPP2). This means that pensionable earnings between $68,500 and $73,200 are subject to secondary CPP2 contributions.

These amounts were calculated in accordance with CPP legislation and account for the growth of average Canadian weekly wages and salaries.

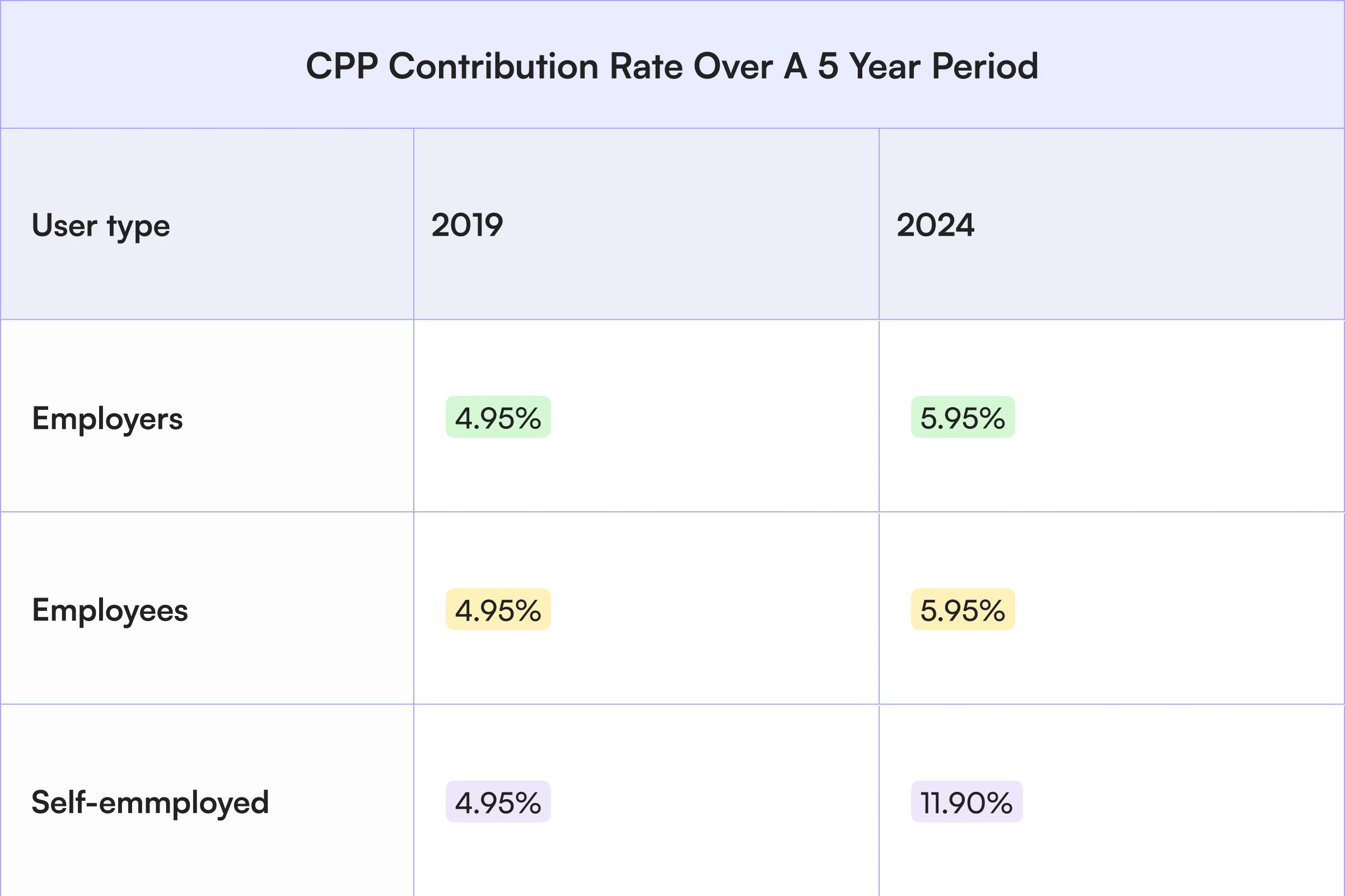

Employer and employee CPP contribution rates for 2024 will remain at 5.95%, and the maximum contribution will be $3,867.50 each, up from $3,754.45 in 2023. The self-employed CPP contribution rate will also remain at 11.90%, and the maximum contribution will be $7,735.00, up from $7,508.90 in 2023.

Employee and employer CPP2 contribution rates for 2024 will be 4.00%, and the maximum contribution will be $188.00 each. The self-employed CPP2 contribution rate will be 8.00%, and the maximum self-employed contribution will be $376.00.

Contributors are not required or allowed to make contributions on pensionable earnings above $73,200.

So how will this work? In 2024, if an employee makes under $68,500, they will not be affected by the second earnings ceiling. Therefore, they will not be subject to make second CPP contributions, only base and first CPP contributions. The employee’s total annual contributions will be their annual salary multiplied by 5.95%. This means you, as an employer, will be responsible for contributing that same amount.

However, if an employee’s salary is higher than the first earnings ceiling, they will make base and first CPP contributions at 5.95%, as well as second CPP contributions (4% on any earnings above $68,500 beginning in 2024). This means your total contributions as an employer will be equal to the total amount of the first contribution amount plus the second contribution amount.

To fully understand the maximum CPP contribution 2024 rates, you’ll also have to understand how the CPP expansion plan will be carried out over the next few years.

The Canada Pension Plan (CPP) and CPP Enhancement

Now that we’ve covered the basics of the Canada Pension Plan and the figures for 2024, let’s discuss the government’s CPP enhancement plan and how it will affect employer contributions not only in 2024, but in the following years as well.

What is The CPP Enhancement Plan?

The Canada Pension Plan (CPP) enhancement, put into effect on January 1, 2019, is a government-backed plan that aims to boost retirement income for employed Canadians and their families.

The CPP consists of:

- The base (or original CPP).

- The first component, which was phased in between 2019 and 2023.

- The second component, which will be phased in between 2024 and 2025.

As it reaches full effect, this enhancement is expected to raise the maximum CPP retirement pension by around 50%. The CPP enhancement plan aims to reduce the number of Canadian families at risk of insufficient retirement savings, especially for those who lack access to a workplace pension plan.

How Will it Be Implemented?

In 2019, the government announced that CPP contribution rates will begin to gradually increase each year over a five-year period to reach a total of 1% by January 1, 2023, for employees and employers. For self-employed individuals, the total increase in CPP contribution rates was 2% as of January 1, 2023.

Before January 1, 2019, employees and employers made base contributions to the CPP amounting to 4.95% of the employee's maximum annual pensionable earnings. This is the base contribution.

During the first stage of the CPP enhancement plan between 2019 and 2023, the employee contribution rate gradually increased from 4.95% to 5.95% over five years. This represents the combined initial base contribution (4.95%) as well as the first additional CPP contribution (1%) that represents the increase to the year’s maximum pensionable earnings (YMPE), also known as the first ceiling.

As of January 1, 2024, a new second tier of maximum pensionable earnings for the year will be introduced. This will allow employers and employees to invest an additional portion of their earnings into the CPP. This new limit is known as the Year’s Additional Maximum Pensionable Earnings (YAMPE) or second earnings ceiling. It will not replace the first earnings ceiling, but will subject worker’s earnings to two earnings limits.

CPP Enhancements for 2024

In 2024, a second earnings ceiling called the year’s additional maximum pensionable earnings (YAMPE), will be introduced. The amount of this second ceiling is determined by the amount of the first earnings ceiling.

Beginning January 1, 2024, employees and employers will each be responsible for contributing an additional 4% on any earnings above the first earnings (YMPE) up to the amount of the second earnings ceiling (YAMPE). These are their second CPP contributions.

The amount of the second earning ceiling is:

- 7% higher than the first earning ceiling in 2024

- 14% higher than the first earning ceiling in 2025 and the following years

The rate of second CPP contributions for self-employed individuals will be 8% of their income earned between the first and second earnings ceiling in 2024.

How Will The CPP Enhancement Plan Affect Employers?

As mentioned already, before 2019, the annual contribution rate stood at 4.95%, with maximum pensionable earnings and the maximum amount for contribution rates increasing marginally each year. However, since the CPP enhancement plan took effect, these rates have been increasing at a faster rate and will continue to do so for the foreseeable future.

Starting in 2024, the second earnings ceiling will be set at 7% above the first earnings ceiling. In 2025, it will be set at a level 14% higher than the first earnings ceiling. From 2026 on, both the first and second earnings ceilings will experience gradual annual increases, while the contribution rates will remain unchanged indefinitely.

These changes may pose some challenges and incur extra costs for employers. This continual increase in rates means employers will need to stay up to date with yearly information released by the Government of Canada regarding changes to yearly contribution rates to remain compliant with local regulations.

This is where an Employer of Record (EOR) may be of help. An EOR is a third-party entity that hires employees on behalf of companies based outside of Canada. The EOR takes on the other company’s employer-related responsibilities and ensures all contract, insurance, banking, tax, and payroll requirements are met. This allows you to compliantly employ and pay hires in Canada without having to set up a new entity.

What Needs to Be Done as an Employer?

Employers will be responsible for:

- Withholding and remitting second CPP contributions the same way as base CPP contributions.

- Reporting employees base and first enhanced CPP contributions in Box 16 on the T4 slip. At the start of the 2024 tax year, employees' second CPP contributions will also need to be reported in Box 16A on the T4 slip.

All employer contributions to the CPP are considered eligible for tax deduction.

What About Employment Insurance (EI)?

Employment Insurance (EI) is a Canadian federal program that offers temporary financial aid to eligible individuals who have lost their jobs and are actively seeking new employment. The program is administered by the Government of Canada.

EI benefits are designed to assist individuals who are temporarily unemployed through no fault of their own, including layoffs, plant closures, or illness.

To qualify for EI benefits, individuals must have worked a specific number of insurable hours and be actively looking for work. Individuals will need to have between 420 and 700 hours of insurable employment during the qualifying period to qualify for EI benefits.

Eligible individuals can receive weekly EI payments for up to 26 weeks (or longer in certain circumstances). The amount they receive is based on their average insurable earnings over the past 52 weeks and is subject to a maximum limit.

According to CPP and EI regulations, both the employer and the employee may have obligations to contribute to CPP when the employee is engaged in pensionable employment, and to EI when the employee is in insurable employment. While employer and employee contributions are equal for CPP, for EI premiums, the employer portion is generally 1.4 times the employee portion.

Employer EI Contribution Rates in 2024

Each year, The Canada Employment Insurance Commission is tasked with establishing the premium rate for the year, which is determined by a seven-year break-even rate projection provided by the EI Senior Actuary. This rate is determined with the aim of generating just enough premium revenue to cover EI expenses over the subsequent seven years, thereby balancing the cumulative surplus or deficit in the EI Operating Account. Any alterations to the premium rate on a yearly basis are constrained by a legal cap of five cents.

In September 2023, the Canadian Government announced the 2024 Employment Insurance (EI) premium rate. The rate will be set at $2.32 for employers who pay 1.4 times the employee rate and $1.66 per $100 of insurable earnings for employees. This is a three-cent increase from the 2023 EI premium rate of $2.28 for employers and $1.63 for employees.

The Commission has additionally stated that the maximum limit of insurable earnings for 2024 will rise to $63,200, up from $61,500 in 2023. This threshold, on which both workers and employers remit EI premiums, is adjusted each year to account for inflation. The highest annual EI contribution for employers will increase by $65.34, totalling $1,468.77 per employee. Workers will see a rise of $46.67, totalling $1,049.12.

For employers, this means additional contributions per Canadian employee. If you have multiple employees located in Canada, you’ll be responsible for making correct contributions on behalf of each employee. You must stay up to date with the yearly changes to the maximum yearly contribution rate for CPP and EI, or else risk non-compliance fines and possible criminal charges.

By partnering with a global Employer of Record (EOR), you can avoid the risk of incorrect contributions. Your EOR will handle all payroll-related taxes and government contributions so you can focus on what’s important.

Plan Ahead with Borderless

Overall, CPP and EI are important components of Canada's social safety net. They are designed to help Canadians maintain a basic standard of living in retirement, as well as during periods of disability, unemployment, or following the death of a loved one.

However, if you are an employer who manages a global workforce, partnering with an experienced Employer of Record like Borderless can prove invaluable to your business. Not only can we help manage yearly contributions to Canada’s ever-changing CPP and EI programs, but we also act as a trusted third party that can help you hire and pay employees in over 170 countries.

Borderless is your number one resource global Employer of Record, contractor management services, global visa and immigration services, and more.

Speak with our team today to get started.

Disclaimer: Borderless does not provide legal services or legal advice to anyone. This includes customers, contractors, employees, partners, and the general public. We are not lawyers or paralegals. Please read our full disclaimer here.